Car refinancing means you replace your current auto loan with a new one. You get a new loan with different terms. People often refinance a car to achieve financial savings. You might want a lower interest rate. A better interest rate can reduce your monthly payments. Refinancing helps you adjust your loan terms. This process empowers you to take control of your car loan. Explore auto refinance options for potential savings and a better rate.

Key Takeaways

Refinancing your car loan means you get a new loan. This new loan often has better terms. It can lower your interest rate and monthly payments.

Refinancing makes sense if interest rates are lower. It also helps if your credit score has improved. You can save money or change your payment plan.

Before you refinance, check your current loan details. Know your credit score. Find out your car’s value. Gather all needed documents.

Compare offers from different lenders. Look at the Annual Percentage Rate (APR). This shows the true cost of the loan. A good credit score helps you get a lower rate.

After you get a new loan, sign the agreement. Make sure your old loan is paid off. Update your car’s registration. Set up automatic payments for your new loan.

What is Auto Refinancing

Defining Refinancing a Car

Refinancing a car means you replace your current auto loan with a new one. You get a new loan, usually with better terms. This process helps you change the conditions of your existing car loan. You might seek a lower interest rate or different payment schedule. The goal is often to improve your financial situation.

Benefits of Refinancing Your Car Loan

Refinancing your car loan offers several key advantages. The primary financial benefits include saving money and providing more flexibility in your budget. You can often secure a lower interest rate. This happens if your credit score has improved or if market rates have decreased since you first got your loan. A lower interest rate directly reduces the total cost of your loan.

One major benefit is reduced monthly payments. Refinancing can free up cash in your budget each month. You can also choose to pay off your loan faster. This means you refinance to a shorter term. Paying off your loan sooner saves you money on overall interest. Some refinancing options even let you access your vehicle’s equity for cash. This provides quick funds if you need them.

Credit unions often provide competitive rates for auto refinance. Their not-for-profit structure allows them to offer better rates than traditional banks. This reduction in interest leads to significant savings over the life of the loan. You can use these savings to free up funds or pay off your loan quicker. Credit unions also offer flexibility to personalize loan terms. You can adjust the loan length to fit your current financial needs. This means you can aim for lower monthly payments or a faster payoff. Many credit unions also have no prepayment penalties. This flexibility allows you to pay off your loan early without extra fees. You save on interest charges and reach your financial goals sooner.

Should You Refinance an Auto Loan

When Refinancing Makes Sense

You should consider if you want to refinance a car in several situations. If current market rates are lower than your original loan’s rate, you can secure a better interest rate. This leads to significant savings. Your credit score may have improved since you first got the loan. A stronger credit profile helps you qualify for more favorable rates and loan terms.

Perhaps you did not shop around much the first time you got your loan. Refinance an auto loan now for a chance to get a better deal. You might want to adjust your monthly payment. Refinancing allows you to modify payments to fit your budget. You can extend the term for lower payments. Or you can shorten it to save on interest and pay off faster. You can also consolidate other debt. If you have vehicle equity, you can combine higher-interest debts into a single, lower-rate auto loan payment. This simplifies your finances and offers potential savings.

Potential Downsides

Refinancing is not always the best choice. You might owe more on your car loan than the car’s current value. Many lenders will not approve this process in this case. Your car might be older, for example, more than 10 years old or over 125,000 miles. Lenders are less likely to approve refinancing due to rapid depreciation.

The amount you need to refinance might be small, less than $7,500. Some lenders have minimum refinancing thresholds. You may have recently purchased the car. New cars depreciate quickly. This could leave you underwater on the loan. Your current auto loan might include prepayment penalties. Refinancing would trigger these fees. This could negate any savings. If you are close to paying off your vehicle, lenders may not want to refinance my car for a small remaining balance.

Credit Score Impact

You might wonder how does refinancing a car loan affect my credit. Applying for auto refinance creates a hard credit inquiry. This can temporarily lower your credit score.

This inquiry stays on your report for up to two years. Its impact usually lasts up to 12 months. FICO models group inquiries within a 14-day period as one. This helps minimize the impact. Refinancing effectively ‘restarts’ your car loan. This can decrease the average age of your credit accounts. This factor makes up 15% of your FICO score. So, its impact may not be huge. Your credit score will significantly impact your ability to get a good interest rate.

A new loan is reported. This indicates a new debt obligation. However, consistent, on-time payments can restore or improve your score. The impact of hard inquiries fades within a year. Refinancing replaces an existing loan with a new one. The impact on your credit score is often minimal.

Prepare to Refinance a Car Loan

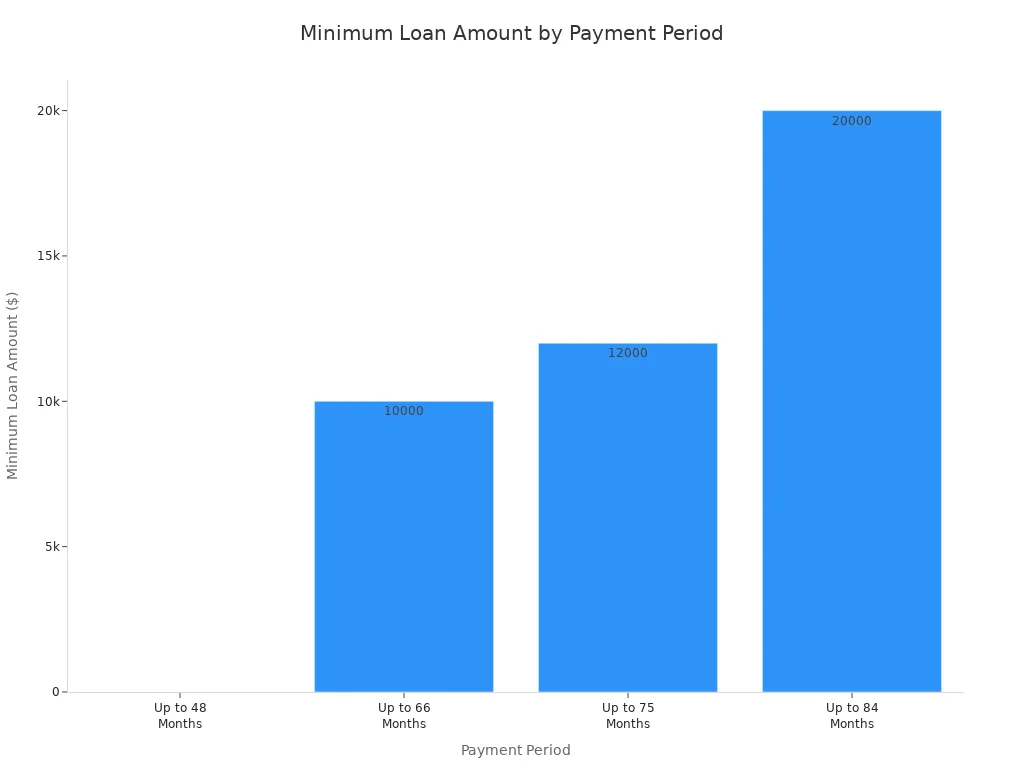

Before you apply to refinance a car loan, you must gather important information. This preparation helps you understand your options. It also ensures a smooth application process. Experts recommend waiting 6-12 months before you refinance a car. This waiting period allows your credit score to recover from the initial loan’s hard inquiries. It also gives you time to establish consistent, on-time payments. This can lead to better APR offers. Lenders also have specific requirements. For example, some lenders have minimum loan amounts based on the payment period you choose.

Payment Period | Minimum Loan Amount |

|---|---|

Up to 48 Months | No minimum loan amount |

Up to 66 Months | $10,000 |

Up to 75 Months | $12,000 |

Up to 84 Months | $20,000 |

Review Current Loan Details

You should first review your current auto loan. Check for any prepayment penalties. Some lenders charge a fee if you pay off your loan early. This fee could reduce your potential savings from refinancing. Compare your current interest rate with the interest rate you could qualify for today. This comparison helps you see if refinancing offers a better rate. Consider how much time remains on your loan. Most auto finance companies require at least 12 months left to refinance. Extending or shortening the loan term will impact your overall interest paid and monthly payments. Also, check the age of your vehicle and how much you still owe. Negative equity can make refinancing challenging.

Check Your Credit Score

Your credit score plays a big role in the interest rate you receive. A higher credit score often means a lower interest rate. You can get your credit score for free from various sources. Review your credit report for any errors. Correcting mistakes can improve your score. Knowing your score helps you set realistic expectations for new loan rates. It also helps you understand the kind of auto loan refinance offers you might receive.

Determine Car Value

Lenders consider your car’s value when you refinance. They want to ensure the loan amount does not exceed the car’s worth. Key factors influence your car’s resale value. These include its incident history, mileage, and wear-and-tear. Brand reputation, buying trends, and model longevity also play a part. You can use online tools like Kelley Blue Book (KBB) or the National Automobile Dealers Association (NADA) to estimate your car’s value. Bookout sheets are crucial for determining a vehicle’s estimated value. They require specific details. You need your vehicle’s make, model, year, and VIN. You also need the total miles traveled. The car’s condition, including its interior, exterior, and mechanical parts, is important. The specific trim, like leather seats or navigation, also matters.

Gather Documents

Lenders require several documents to process your auto refinance application. You will need a valid, government-issued driver’s license. Provide your vehicle’s up-to-date registration. An odometer photo showing your car’s mileage on the application date is often necessary. You must also show proof of auto insurance. This documentation confirms you have a valid and active car insurance policy meeting state requirements. Lenders typically require proof of income. This shows your ability to repay the loan. You can use pay stubs from the last month, bank statements, or a W-2. Self-employed individuals might need to provide a 1099, profit and loss statement, or bank statements. Proof of residence is also mandated by federal law. A utility bill, mortgage statement, or lease agreement can serve as proof. If you live in a state where you hold the title, you will need your vehicle title. You will also need title transfer documents. These authorize the lender to file the auto lien.

Shop for Loan Offers

You have prepared your documents and checked your credit. Now, you are ready to find the best auto refinance loan. This step is crucial for securing potential savings. You need to compare offers from different lenders. This helps you find the best terms for your new loan.

Compare Lenders

You have many options when you look for a new loan. Different types of lenders offer auto refinance services. You can find these services at traditional banks. Credit unions also provide competitive rates. Online lenders offer quick and easy processes. For example, Ally is an online financial institution. It offers auto loan refinancing. You can pre-qualify in minutes. This does not impact your credit score. You could save money on monthly payments. Credit unions like LAFCU also offer vehicle loans. They often have refinancing options for their members.

It is smart to compare offers from each type of lender. Each one has different strengths.

Feature | Banks | Credit Unions | Online Lenders |

|---|---|---|---|

Interest Rates | Lower maximum rates, potential for relationship discounts | Often even lower than banks, capped at 18% for federal credit unions | Lower starting rates, but higher maximum rates |

Application Process | Slower, may not offer prequalification, potentially requires in-person visits | Easier once a member, but may have limited digital tools | Faster, typically offers prequalification, fully online |

Eligibility | Stricter requirements, difficult for bad credit or limited history | May have tighter lending standards, requires membership | Looser eligibility, better for limited or damaged credit |

Customer Service | In-person service available, highly regulated | Member-focused, personalized service, often fewer branches | Primarily digital, convenient |

Technology | Digital banking options, but some may not offer prequalification | Fewer digital banking tools compared to large banks | Built for speed and convenience, fully online processes |

Overhead | Higher due to physical branches | Lower due to non-profit status | Lower due to no physical branches, savings passed to customers |

Funding Speed | Longer processing time | Can be slower due to smaller size | Faster, potentially same-day funding |

Membership | Not required | Required, may have specific criteria | Not required |

You should compare offers from several lenders. This helps you find the best fit for your needs.

Understand Loan Terms

When you compare offers, you must look beyond just the monthly payment. You need to understand all the loan terms. These details affect your total cost and your financial flexibility.

Here are the key loan terms you should compare:

Annual percentage rate (APR): This is the true cost of borrowing money. It includes the interest rate and other fees.

Interest rate: This is the percentage lenders charge you for borrowing money.

Length of the loan: This is how long you have to pay back the loan. It is also called the loan term.

Total amount financed: This is the total amount you borrow.

Amount of the loan: This is the principal amount you are borrowing.

Monthly payment: This is the amount you pay each month.

You also need to compare rates and fees. Some lenders charge fees for refinancing. These fees can add to your total cost.

Common fees you might see include:

Early Termination Fee: Your current auto loan might have this. It is a penalty if you pay off your original loan early.

Transaction Fees: These are costs for processing your old loan and starting your new loan.

State Registration Fees: Some states require you to re-register your vehicle. These fees vary by state.

Late Payment Fees: You pay these if you do not make your monthly loan payments on time.

Regulatory Fees: These are paid to the state government.

Origination Fees: You pay these to the lender for setting up the loan.

Title Transfer Fee: This updates the lienholder information on your car’s title.

Re-registration Fee: Some states require this when you refinance with a new lender.

Application Fees: Lenders charge these to process your application. Many auto refinance lenders waive these.

Prepayment Fees: These are charged for paying off a loan early. They are uncommon for auto loans.

Always ask lenders for a full breakdown of all costs. This helps you compare rates and fees accurately.

Look for Best Rates

Your goal is to find the lowest interest rate. A lower interest rate means you pay less money over the life of the loan. Several factors influence the interest rate you receive. The federal funds rate affects general auto loan rates. This rate is set by the Federal Reserve. It impacts the interest rates lenders offer.

Other factors also play a role:

Credit Scores and History: Lenders check your creditworthiness. A higher credit score usually means a lower interest rate.

Income and Debts: Lenders look at your ability to repay the loan. They check your income and existing debts.

Loan Amount: The total amount you want to borrow can affect the interest rate.

Loan Term: The length of time you take to repay the loan impacts the rate. Shorter terms often have lower rates.

Down Payment: The money you pay upfront can influence the rate.

Vehicle Type: Whether your car is new or used can also be a factor.

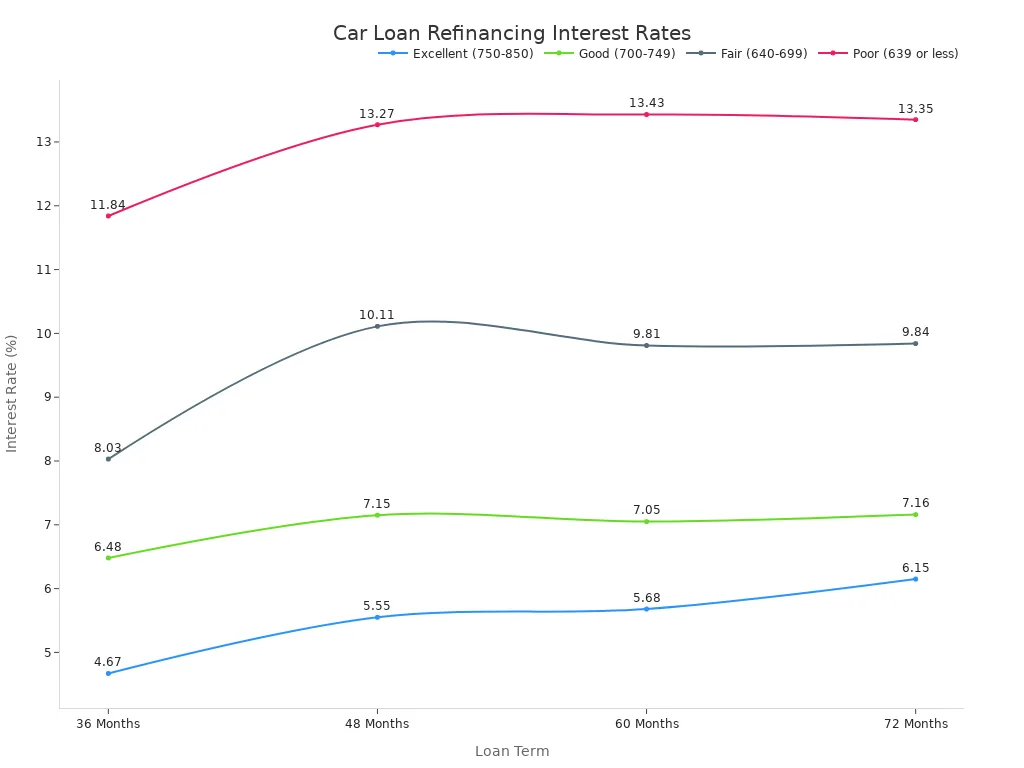

You should compare rates on auto refinance offers. Look at the Annual Percentage Rate (APR), not just the interest rate. The APR gives you the true cost.

Here is a general idea of current interest rates for auto refinance:

Loan Term | Excellent (750-850) | Good (700-749) | Fair (640-699) | Poor (639 or less) |

|---|---|---|---|---|

36 Months | 4.67% | 6.48% | 8.03% | 11.84% |

48 Months | 5.55% | 7.15% | 10.11% | 13.27% |

60 Months | 5.68% | 7.05% | 9.81% | 13.43% |

72 Months | 6.15% | 7.16% | 9.84% | 13.35% |

You can see that your credit score greatly affects the rate you get. A good credit score helps you secure a lower interest rate. Always compare offers from several lenders to find the best rate for your situation. This can lead to significant savings over your current auto loan.

Apply for Your New Loan

You have compared offers and found a great option. Now, you are ready to apply for your new loan. This step moves you closer to saving money on your car.

Complete Application

You will fill out an application form for your new loan. This form asks for important details about you and your vehicle. You will provide your driver’s license information. You also need to share details about your current vehicle registration and auto insurance. Lenders ask for proof of mileage, like an odometer photo. You will also give information about your car, such as its make, model, year, and Vehicle Identification Number (VIN). The application will also ask for the payoff amount for your current auto loan. This helps the new lender know how much to pay off.

Submit Required Information

After completing the application, you must submit supporting documents. These documents confirm the information you provided. You will need proof of residence. This can be a utility bill, a mortgage statement, or a phone bill. You also need proof of income. If you are an hourly or salaried employee, provide pay stubs from your last two pay periods. Freelancers or self-employed individuals typically submit tax returns from the last two years. Lenders may also ask for other specific documents, like a green card or social security card. Providing these documents quickly helps speed up the process.

Review Loan Offer

Once you submit everything, the lender will review your application. They will then send you a final loan offer. Carefully review all the terms of this new loan. Check the interest rate and the length of the loan. Make sure the monthly payment fits your budget. The process to refinance a car loan can take anywhere from a few hours to two weeks. Some lenders, like LendingClub, state it may take up to 15 business days. Providing all requested documents promptly helps to get your new loan finalized faster. This new rate can save you money compared to your current auto loan.

Finalize Your Refinance

You have found a great new loan. Now, you must complete the final steps. This ensures your refinance is successful.

Sign New Agreement

You must carefully review all terms before you sign any new loan agreement. Do not feel rushed. Make sure you see all fees and charges clearly. This helps you avoid unwanted additions. Once you sign the car loan agreement, its terms become legally binding.

Neither party can change them without the other’s clear consent. Dealers cannot legally alter a signed contract without your knowledge. Such changes violate contract law. Be watchful for differences between verbal promises and written terms. Also, look for unexplained changes in payment structures. You might see additional fees not discussed before. If you find unauthorized changes, document everything. Contact the dealer in writing for correction. You can also seek legal action. Always get a signed copy of the completed credit contract. Do not leave without it. After financing, the creditor holds a lien on your car’s title. This lasts until you fully pay the loan. Late or missed payments can lead to serious problems. These include late fees, repossession, and negative impacts on your credit report.

Old Loan Payoff

Your new lender typically pays off your old loan directly. In some cases, you might receive the loan funds. Then, you are responsible for paying off the old loan yourself.

If you are responsible, contact your old lender. Request a payoff letter. Schedule the payment to your old lender. Follow up to ensure the old account is closed. Continue making payments on your original loan until you are certain your new lender has paid it off. If you overpay, the old lender will refund the difference. Ensure the original loan is paid off in full.

Update Registration

Updating your vehicle title with the new lender’s name is a crucial step in your auto refinance. You will upload proof of registration for the car you refinanced. Make sure it is current and all fees are paid. You will also mail title transfer documents. These allow the new lender to transfer the car title from the previous lender. You might complete a limited power of attorney (LPOA) form. This form authorizes the title transfer. You will print and sign this form. It may need notarization.

Manage Your New Loan

Set Up Payments

You have successfully completed your auto refinance. Now, you need to manage your new loan effectively. Setting up your payments is the first step. You have several options for making payments on your loan. You can choose any of the following methods that are convenient for you:

Online Payments: Pay directly through your lender’s website.

Automatic Payments: Set up recurring payments from your bank account.

Mail a Check: Send a check through the postal service.

Phone Payments: Make a payment over the phone.

Setting up automatic payments is highly recommended. This ensures your loan payments are always made on time. Timely payments are vital for maintaining a good credit score. They also help you avoid late fees.

By ensuring punctual payment history, automatic payments keep your credit score intact. Late or missed payments can significantly damage your credit. Automatic payments prevent costly late fees and penalties. They simplify your financial management. You do not need to remember due dates. This frees up time for other financial tasks. Automatic payments provide peace of mind. You know your payments are handled. Some lenders even offer reduced interest rates for setting up automatic payments. This can lead to potential savings over the loan’s lifetime.

Monitor Progress

After setting up your payments, you should regularly monitor your loan progress. Check your monthly statements. Make sure all payments are applied correctly. You can often view your loan balance and payment history online. This helps you track how much you still owe. It also shows you how much interest you have paid. Monitoring your loan helps you stay on top of your finances. You can ensure you are on track to pay off your refinance loan as planned. If you notice any discrepancies, contact your lender immediately. Staying informed about your loan helps you maintain financial control.

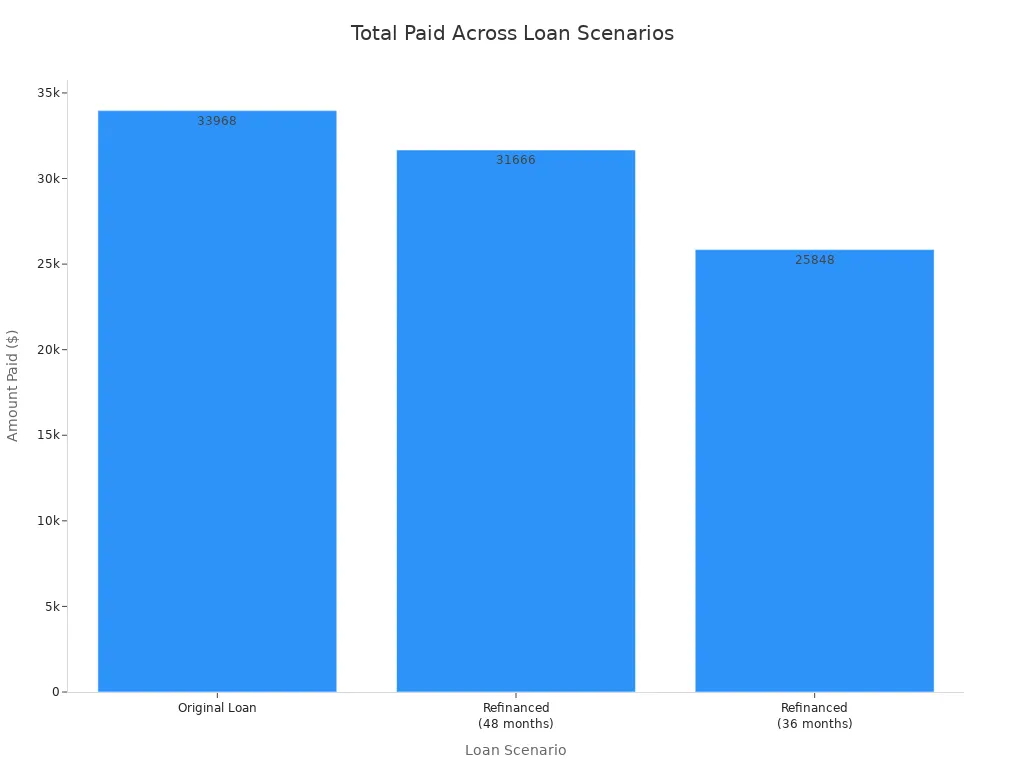

Refinancing your car loan offers significant savings and improves your financial health. You can secure a lower interest rate, reducing your total interest paid over the loan’s life. This leads to substantial savings. For example, look at these potential savings:

Scenario | Original Loan | Refinanced (48 months) | Refinanced (36 months) |

|---|---|---|---|

Loan Amount | $30,000 | $24,583 | $24,583 |

Term | 60 months | 48 months | 36 months |

Rate | 5.00% | 3.25% | 3.25% |

Monthly Payment | $566 | $547 | $718 |

Total Paid (Life of Loan) | $33,968 | $31,666 | $25,848 |

Total Savings (vs. Original) | N/A | $2,302 | $1,320 |

Total Savings (vs. 48-month refinance) | N/A | N/A | $408 |

The process involves preparing your documents, shopping for loan offers, applying for your new loan, and finalizing the refinance. Take action to explore your auto refinance options. You can gain control over your car loan and secure a better financial future.